This week, I’d like to share how I use my Bullet Journal for financial planning, which I call “Mindful Money”.

To be clear, this has nothing to do with the book Mindful Money: Simple Practices for Reaching Your Financial Goals and Increasing Your Happiness Dividend by Jonathan K. DeYoe. I only am keeping the title the same because it’s what my Bullet Journal spread on it is titled.

The Basics

- Break down ALL of your transactions into 6 categories and color-code:

-

- Necessities

- As Needed

- Limited

- Very Limited

- Unless Out

- Do Not Buy

- Within the categories, plan transactions with specific limits, whenever necessary.

- Track transactions throughout each month in the habit tracker, to show which days money was spent in which category.

- List transactions individually in a spreadsheet, and use the same color-code to show trends in transaction categories. (Other things happen with this spreadsheet, but we’ll get to that later.)

The Categories

Necessities – This is where all your regular, boring expenses go like your bills, groceries, gas, payments on debts, etc. I like to include groceries and gas in this category because (1) I can’t control the price of gas, and I have to go to work, so I can’t truly put a limit on the amount I spend on it, and (2) I think food prepared and/or eaten at home is always going to be more cost-effective than eating out, so I choose not to limit this. I also noticed recently that I tend to spend about the same on groceries every month, even without trying to stick to a strict grocery budget, so I am leaving it in Necessities. I’ve built in a way to show your monetary limits on these expenses in the spreadsheet if that helps you to stick to more specific amounts.

As Needed – This is where things like gifts, postage, travel expenses, and repairs go. This category is the strangest for me, because it’s sort of a “free-pass” on a few things, like being able to spend what’s needed if I’m traveling, and also a catch-all for the unexpected things in life, like having to repair a cracked phone screen. However, I have committed to taking the “as needed” title of the category very seriously, so I’m only allowing expenses in that category to be truly necessary to what is going on, but not so necessary that they’re regular expenses like the first group.

Limited – This category is where things start to get more specific. Take a look at your expenses and see where you are spending more than you would like to and pick those that you know you can’t eliminate, but can definitely reduce. Remember to be realistic about what goes in each group, and also to be specific about the limits you set. For Limited, I picked going out to lunch and dinner, getting coffee (which includes pastries or whatnot in the same transactions), going to the movies, and going through the car wash, and set a strict times or amount per ____ on each of them. For movies, I decided to make that a “rolling” limit, which means I can see up to 24 movies at the theater within the year, but stick to 2 a month. In January, I only saw one movie, so I can see up to 3 in February, or save some or all of them for March, and so on.

Very Limited – In this category, list things that you tend to buy on impulse and put limits on them to help curb that spending. For me, this is clothing and cosmetics. This means I need to take a good look at my closet before purchasing something new and (1) get rid of things I’m not wearing and donate them (I love Thred Up for this!) and (2) make sure I’m not buying something I basically already have. I also recognized my weaknesses for certain brands and habits, like how much I love popcorn at the movies or how I will always buy LORAC PRO palettes and most KathleenLights collabs/some KL polish colors – but they’ve gotta be on sale!

Unless Out – For this category, I recommend taking stock (literally, if you must) of the things you have in your home and figure out some things that you need to use up before buying a lot more. Maybe you used to coupon and need to use up your stash of toothpaste and hand soap before buying anything new, or maybe you’re like me and have an excessive amount of makeup in some categories, but only have one favorite foundation you’ll need to repurchase as the year goes along. It’s unlikely that I’ll run out of a lot of the things on this list, especially “journal stuff” (unless all of my Sharpie Pens disappear into the pen abyss) but for things like “skincare”, I know I’ll probably run out of my daily moisturizer in a few months, and I’m happy to not feel a lot of guilt for purchasing something that I need, while limiting myself from purchasing stuff I simply just want at the moment.

Do Not Buy – In my opinion, this should be the smallest category, since it’s really hard to say that you will not buy something in an entire year and hold yourself to that. This plan is supposed to be set up for your success! For me, I know I have plenty of music in my library, especially when considering services like Spotify and Pandora, so I probably could have put “new music” on Do Not Buy, but I also knew that Fall Out Boy was about to release an album, and there was no way I was not going to buy that, so I limited it to purchasing new music only from my very favorite artists, which will keep me from randomly buying musical soundtracks, one-off songs I hear on the radio, or an excess of the back catalog of bands I love, but don’t already own their older stuff. (I also think buying music could be a good way to reward myself as I progress through the year, so that’s another reason I kept it out of the DNB category!)

Incorporating this plan in your Bullet Journal

Having a “mindful money” page with the breakdown of the six categories has been a really helpful reference as I consider purchases.

Start out with your basic list, but don’t be afraid to make adjustments as you go. I started out January pretty confident that I had everything I’d need to split up down on paper, but I added a few things throughout the month. For example, I added “Car Wash 1x/Month” to the Limited category since I know this is something that I need, but not something that shouldn’t be restricted somewhat. I also added “Repairs (car, phone, etc.)” to the As Needed category, because that’s something that truly can’t be planned for, especially if it’s a repair that needs to happen immediately.

Next, track the basics in your habit tracker – what categories did you make purchases in each day? This gives an overall look at how the categories break down and when you’re having true “No Spend” days.

I kept having to flip back to the main page to remember the different categories, so for February, I redid how I set up the tracker. As I get more comfortable with the system, I’ll probably go back to just the colored dots.

Other Helpful Bullet Journal Pages

If you want to take it a step further, you can include a page for savings goals and debt or savings tracking, to give a visual reminder of your progress. These don’t really get incorporated into my planning, but they help to guide my decisions on making (or not making) some purchases. (Sorry for all the blackout, but I wanted to show how the spread is set up, but not the personal info!)

I also highly recommend creating a page like this next one if you want to break the habit of eating out often. This page has helped remind me the true cost of going out to eat at the go-to places my husband and I usually pick. It’s inevitable that we’re going to go out from time to time, which is built into the Limited category of the plan, but this helps me to think about what to choose depending on what we have to spend at the time.

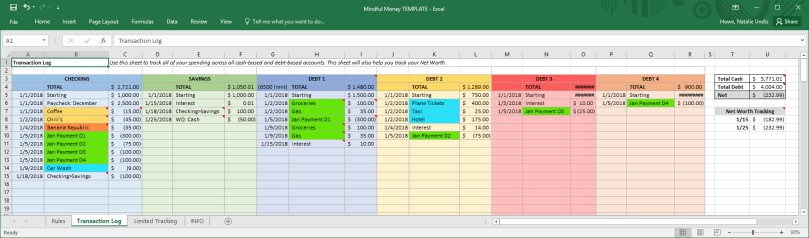

The Spreadsheet

Alongside my journal, I use a spreadsheet to track all transactions across my cash accounts and debts. I’ve created a template version for you to use, if you’d like to try out my technique yourself. You can use this spreadsheet alone, or along with your Bullet Journal! Click Here to Download the FREE Mindful Money Template!

I’ve included a lot of comments in the sheet to give additional tips for using it, but here’s a brief overview of how I make it work for me with some category ideas and example transactions to get you started.

This first page, the Rules sheet, is where you should list out all the details of the six categories. On my spreadsheet, I’ve included a bit more than I do in the journal. This is because the journal may be viewed by others sometimes, so I don’t like to list things like the specific amounts of some of my Necessities, and because there’s more space to write details of why certain things are limited the way that they are.

On the Transaction Log sheet, list out your cash accounts (debit and savings) and debts (credit cards, medical bills). I choose not to include my investment account in this sheet since I only use that for home and retirement savings. I’ve included a few example transactions in this sheet to get you started, and to share some comments on how to use the sheet to its maximum potential.

The most important part of this is how you list the transaction amounts. For cash accounts, purchases are negative (-) and deposits are positive (+), whereas in debts, purchases are positive (+) and payments to the debt are negative (-). It’s set up this way so you can see your total net worth across all accounts and debt. Seeing this number change over time has been one of the greatest motivators for sticking to my plan!

Last, use the Limited Tracking sheet to help see both the number of times and the amount of money you’re spending on your Limited category purchases like dining out, coffee, etc.

![]()

Note: I do realize I could probably accomplish something similar in an app like Mint, but I’ve used that for so long with a different set of categories that I don’t want to mess that history up. If you haven’t tried out Mint yet, and you want to apply these categories to your planning in there, I think that would be an awesome idea!

Please let me know if you try out this method! I would love to see how others adapt it to their needs and situations. Post your thoughts, questions, and ideas about managing your money in your bullet journal below!

– Natalie

P.S. Here’s some referral links to some of my favorite sites. Use if you’d like!

- Ebates – This is a great way to earn cash back from online shopping (that you’re already doing) at many of your favorite stores! (Including Sephora & Ulta!) If you join through this link and make a purchase of $25 or more, you’ll get an extra $10 cash back and I’ll get $15, as well as your own referral code.

- thredUP – I love using thredUP to clean out my closet and shop for new pieces at a discounted price – sometimes they’re even brand new with tags! When you join thredUP through this link, you get $10 to spend and I get $10 to shop after you place your first order.

- StitchFix – This is a great way to try out some new items for your closet, without the hassle of going to the stores and the bonus of a personal stylist. If you sign up with this link, you’ll get a FREE styling fee (usually $20) on your first Fix, and I’ll get $25 credit once it ships.

[…] I am officially almost through two full months of filling in my tracker every single day, and I’m probably more proud of myself for that than I should be! I never figured out what to do with the blank page opposite the tracker during February, but as I was setting up for March, I had a breakthrough! I decided to move the expenses part of my tracker over to the opposite page and left some space for notes to help remind me what I purchased each day & why. I think this could help increase the self-accountability that I’m going for with my mindful money plan. […]

LikeLike